The Commonwealth corruption conference and anti-corruption summit in London last week saw the full engagement of civil society. Leaders from big household name NGOs were active online and in person, taking the opportunity to challenge a range of related injustices. It was exciting and encouraging, but these events should prompt those NGOs to ask themselves, ‘how effective are our own organisational counter-fraud and corruption frameworks?’ If the question needed underlining, we also learned that the US government is investigating allegations of corruption affecting NGOs in the Syria emergency response.

What Boards need to do in order to reduce fraud and corruption risk is well-trodden ground. But for international NGOs, one of the great challenges can, in fact, be the Board. As your organisation’s counter-fraud lead, what do you do if members of your Board don’t recognise that fraud and corruption is a problem? Or merely give it lip service, unwilling to invest in meaningful risk reduction efforts? Or worse, are content to turn a blind eye to the risk of physical assets, funds and stock falling into the wrong hands if most aid gets through?

Obtaining the buy-in of an NGO’s Board isn’t about selling them a product – we need their ongoing support and ownership. It’s about changing perspectives; a long haul, not a quick win. So, in helping to generate that ongoing support, I’ve found that these tips (which are not exhaustive and in no particular order) have assisted my colleagues and I; perhaps they might help you too.

1. Educate to effectuate

Fraud and corruption has, historically, not been well understood in this sector. Your Board may have a low or rudimentary understanding of the risk and how to respond to it. This means starting at a basic level, making no assumptions, taking the time to address myths and misconceptions and playing a longer game. ‘Educate as you go,’ Willie Oelofse from Deloitte Kenya told NGOs at a conference in January. As we do so, of course, it’s important to remember that counter-fraud is a good news topic – your organisation may be at high risk, but actually there’s a lot that can be done to reduce it. Boardrooms are learning environments too.

Fraud and corruption has, historically, not been well understood in this sector. Your Board may have a low or rudimentary understanding of the risk and how to respond to it. This means starting at a basic level, making no assumptions, taking the time to address myths and misconceptions and playing a longer game. ‘Educate as you go,’ Willie Oelofse from Deloitte Kenya told NGOs at a conference in January. As we do so, of course, it’s important to remember that counter-fraud is a good news topic – your organisation may be at high risk, but actually there’s a lot that can be done to reduce it. Boardrooms are learning environments too.

2. Keep it simple

Board members are busy. NGOs (especially humanitarian agencies) are often very responsive, and Board members’ attention is divided between competing thematic risk areas and arising issues. Use your time with them wisely. Proposal documents and assessments, for example, should be short or with executive summaries. Don’t bury key messages in a risk assessment document the size of a telephone directory.

3. Speak from within

Civil society is under attack the world over, and the issue of their fraud and corruption exposure can be something that sends Board members running for their shields and helmets – especially if it is perceived to come from an out-group rather than in-group. Take charge of how the matter is framed. Don’t let them entrench in defensive positions to ‘fend off’ your ‘attack,’ or sit in a ‘prospective client’ chair to listen to you ‘pitch’. Instead, use their business language, show your understanding of the difficulties they face, and speak from inside their group. Explain the landscape around them, and how you can help them navigate across it.

Civil society is under attack the world over, and the issue of their fraud and corruption exposure can be something that sends Board members running for their shields and helmets – especially if it is perceived to come from an out-group rather than in-group. Take charge of how the matter is framed. Don’t let them entrench in defensive positions to ‘fend off’ your ‘attack,’ or sit in a ‘prospective client’ chair to listen to you ‘pitch’. Instead, use their business language, show your understanding of the difficulties they face, and speak from inside their group. Explain the landscape around them, and how you can help them navigate across it.

4. Remember that they’re individuals

People make decisions differently and on the basis of different values. For example, I am a big fan of the MBTI, which is one of a range of models that can help us to understand how we like to work and how best to relate to others. Models like these can really help to improve workplace relationships. So try to understand each member of your Board as a person, and what really drives their decisions. Some will be persuaded by cold, hard data, others by less tangible matters such as how your agenda relates to values, supports people, and so on.

People make decisions differently and on the basis of different values. For example, I am a big fan of the MBTI, which is one of a range of models that can help us to understand how we like to work and how best to relate to others. Models like these can really help to improve workplace relationships. So try to understand each member of your Board as a person, and what really drives their decisions. Some will be persuaded by cold, hard data, others by less tangible matters such as how your agenda relates to values, supports people, and so on.

5. Bring the risk to life

Fraud and corruption, especially at a strategic level, can be abstract concepts. Help the Board to connect by painting a picture of the risk with case studies. If you don’t have any in your own organisation, then perhaps partners, donors or other organisations have some they will let you use? If not, then find cases in the public space affecting comparable organisations. If you’re really struggling, consider using fictional examples – but remember to state that they’re fictional!

Fraud and corruption, especially at a strategic level, can be abstract concepts. Help the Board to connect by painting a picture of the risk with case studies. If you don’t have any in your own organisation, then perhaps partners, donors or other organisations have some they will let you use? If not, then find cases in the public space affecting comparable organisations. If you’re really struggling, consider using fictional examples – but remember to state that they’re fictional!

6. Show the benefits

NGO Boards are often allergic to anything with a whiff of extra expense, especially if it is ‘overhead’ or ‘administration’ flavoured. So explain the benefits of the agenda not just in terms of what it prevents, but also what it gains – efficiency, effectiveness, quality improvement, and so on. Much of counter-fraud work synergises with good management (an example arises from the world of retail – smiling as a customer enters not only deters shoplifting by making the individual feel noticed, but is also good customer service!).

NGO Boards are often allergic to anything with a whiff of extra expense, especially if it is ‘overhead’ or ‘administration’ flavoured. So explain the benefits of the agenda not just in terms of what it prevents, but also what it gains – efficiency, effectiveness, quality improvement, and so on. Much of counter-fraud work synergises with good management (an example arises from the world of retail – smiling as a customer enters not only deters shoplifting by making the individual feel noticed, but is also good customer service!).

7. Take an evidence-based approach

NGO Boards manage a lot of risks, only some of which materialize. Using evidence helps them to appreciate how fraud and corruption sits, whether that evidence is perception-based, representative sampled, or from other diverse sources. Cast the evidence net wide – consider staff surveys (especially anonymous surveys), risk assessments, project and programme evaluations, audit reports, security reports, academic research and open source. This may mean that you need to start by improving the detection of incidents, in order to gather enough material. Be cautious with the use of quantification estimates, as these can be inherently open to challenge by those feeling resistant, and with over-stating the case (being debunked seriously damages credibility). Remember to cater for any risks created by the counter-fraud agenda, and to consider any donor or legal obligations.

NGO Boards manage a lot of risks, only some of which materialize. Using evidence helps them to appreciate how fraud and corruption sits, whether that evidence is perception-based, representative sampled, or from other diverse sources. Cast the evidence net wide – consider staff surveys (especially anonymous surveys), risk assessments, project and programme evaluations, audit reports, security reports, academic research and open source. This may mean that you need to start by improving the detection of incidents, in order to gather enough material. Be cautious with the use of quantification estimates, as these can be inherently open to challenge by those feeling resistant, and with over-stating the case (being debunked seriously damages credibility). Remember to cater for any risks created by the counter-fraud agenda, and to consider any donor or legal obligations.

8. Align with organisational objectives and strategy

Just as is the case with private and public sector organisations, the counter-fraud agenda needs to directly support the organisation’s mission. This needs to be clearly elucidated so that Boards can see that counter-fraud is a mainstream activity, rather than a distraction.

Just as is the case with private and public sector organisations, the counter-fraud agenda needs to directly support the organisation’s mission. This needs to be clearly elucidated so that Boards can see that counter-fraud is a mainstream activity, rather than a distraction.

9. Obtain a sponsor

In March’s Charity Finance magazine, I explained why fraud and corruption needs to be a standing priority for NGO Boards. But in addition to this, the counter-fraud agenda needs a champion at Board level. Benefits of this include how the champion can look out for synergies with other business areas as they’re discussed.

In March’s Charity Finance magazine, I explained why fraud and corruption needs to be a standing priority for NGO Boards. But in addition to this, the counter-fraud agenda needs a champion at Board level. Benefits of this include how the champion can look out for synergies with other business areas as they’re discussed.

10. Put in the legwork

A ten-minute agenda item at a Board meeting is not enough to ensure that a Board truly embraces counter-fraud and corruption. Obtain regular meetings with each member to explore their own position and build their buy-in – especially before key decisions are to be made. Similarly, the counter-fraud agenda needs to align not just to the organisation’s mission but to the agendas of those individual Board members. How does countering fraud help, not hinder, the aims of the person in front of you?

A ten-minute agenda item at a Board meeting is not enough to ensure that a Board truly embraces counter-fraud and corruption. Obtain regular meetings with each member to explore their own position and build their buy-in – especially before key decisions are to be made. Similarly, the counter-fraud agenda needs to align not just to the organisation’s mission but to the agendas of those individual Board members. How does countering fraud help, not hinder, the aims of the person in front of you?

11. Bonus tip!

Why not get the members of your Board a copy of Fighting Fraud and Corruption in the Humanitarian and Global Development Sector? It explains the risk, busts myths and misconceptions, and sets out ways for NGOs to minimise the risk. It’s out now with by Routledge, pick up a hardback or e-reader copy via the Routledge website or Amazon!

Anonymous donors are a normal feature of fundraising. We’ve all popped a few coins into a collection bucket. But where NGOs receive unusual or significant funds, with no information on their provenance, a red light should flicker into life. Anonymous giving could be the starting point for a number of laundering methodologies, perhaps even involving insiders. NGOs need to take reasonable steps to identify the sources of such contributions.

Anonymous donors are a normal feature of fundraising. We’ve all popped a few coins into a collection bucket. But where NGOs receive unusual or significant funds, with no information on their provenance, a red light should flicker into life. Anonymous giving could be the starting point for a number of laundering methodologies, perhaps even involving insiders. NGOs need to take reasonable steps to identify the sources of such contributions. An example might arise from the UK. In 2013, the Charity Commission

An example might arise from the UK. In 2013, the Charity Commission  Let’s say you are running a social development enterprise. A company approaches you to purchase a quantity of your beautiful wooden products. You’re delighted – but then the company asks if a second company can settle the invoice on its behalf. They’ll settle up between themselves, later, it says. The red light should come on.

Let’s say you are running a social development enterprise. A company approaches you to purchase a quantity of your beautiful wooden products. You’re delighted – but then the company asks if a second company can settle the invoice on its behalf. They’ll settle up between themselves, later, it says. The red light should come on. Let’s say that our rich, local businessman approaches you with a proposition. He wishes to store some money in a savings account, but he doesn’t like banks. Maybe he says they’re greedy and corrupt, and he wants to help those who live out his own commitment to social justice. He suggests giving you his US$100,000 – which he will retrieve in six months, while you get to keep the interest. Red light.

Let’s say that our rich, local businessman approaches you with a proposition. He wishes to store some money in a savings account, but he doesn’t like banks. Maybe he says they’re greedy and corrupt, and he wants to help those who live out his own commitment to social justice. He suggests giving you his US$100,000 – which he will retrieve in six months, while you get to keep the interest. Red light. A range of complex issues face NGOs that move funds into and around locations of elevated risk, such as conflict zones, fragile states and areas of significant terrorist activity. One of these is that we don’t know who else’s money an MTO is moving in or out of these places. If our NGO engages an unscrupulous, unregulated or badly-run MTO, there are real risks of breaching the principle of ‘do no harm’ and of reputational impact.

A range of complex issues face NGOs that move funds into and around locations of elevated risk, such as conflict zones, fragile states and areas of significant terrorist activity. One of these is that we don’t know who else’s money an MTO is moving in or out of these places. If our NGO engages an unscrupulous, unregulated or badly-run MTO, there are real risks of breaching the principle of ‘do no harm’ and of reputational impact.

This presents a very challenging issue for NGOs that work in high-risk areas, and one with significant tensions at its heart. These include the tension between minimising the risk of diversion versus disrupting the delivery of aid, competing obligations on the ground, and the wider balancing act between regulation and enforcement versus guidance and capacity building.

This presents a very challenging issue for NGOs that work in high-risk areas, and one with significant tensions at its heart. These include the tension between minimising the risk of diversion versus disrupting the delivery of aid, competing obligations on the ground, and the wider balancing act between regulation and enforcement versus guidance and capacity building. Audit is a helpful process that

Audit is a helpful process that  In

In  In 2015, the UK government issued guidance describing the risk of a prosecution for a terrorism offence as a result of involvement in humanitarian efforts or conflict resolution as ‘

In 2015, the UK government issued guidance describing the risk of a prosecution for a terrorism offence as a result of involvement in humanitarian efforts or conflict resolution as ‘ Implied assurance of non-prosecution is always caveated, is not always made by those with the correct authority, and might not relate to that which is perceived. The British guidance note, for example, does not indicate whether it is referring to placing resources in the hands of terrorists (potentially s15-18 Terrorism Act offences), failing to have sufficient systems to prevent sanctions breaches (potentially a s34 Terrorist Asset Freezing Act offence of neglect), failing to report a suspected funding offence (s19 Terrorism Act), or some of those, or none – and so on. In any event, any decisions would be made on the basis of the prevailing circumstances of the case and it is worth noting that Save the Children International were investigated by the Metropolitan Police for

Implied assurance of non-prosecution is always caveated, is not always made by those with the correct authority, and might not relate to that which is perceived. The British guidance note, for example, does not indicate whether it is referring to placing resources in the hands of terrorists (potentially s15-18 Terrorism Act offences), failing to have sufficient systems to prevent sanctions breaches (potentially a s34 Terrorist Asset Freezing Act offence of neglect), failing to report a suspected funding offence (s19 Terrorism Act), or some of those, or none – and so on. In any event, any decisions would be made on the basis of the prevailing circumstances of the case and it is worth noting that Save the Children International were investigated by the Metropolitan Police for

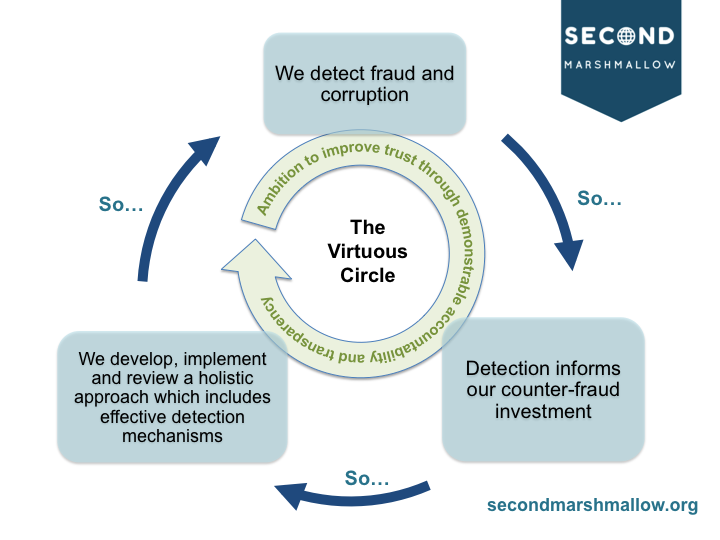

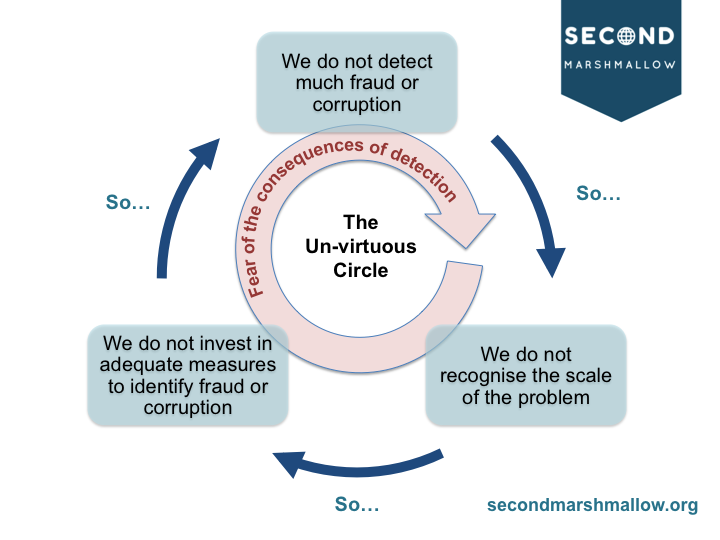

Another way to think of this concealed drainage is like corrosion under your car – unless you go looking for it, you won’t ever realise its presence, scale and danger… until your car falls apart in the middle of the motorway. You may fear the consequences (e.g. costs involved) of detecting the corrosion and needing to deal with it, but these costs in the long run are less than those that the motorway incident might involve.

Another way to think of this concealed drainage is like corrosion under your car – unless you go looking for it, you won’t ever realise its presence, scale and danger… until your car falls apart in the middle of the motorway. You may fear the consequences (e.g. costs involved) of detecting the corrosion and needing to deal with it, but these costs in the long run are less than those that the motorway incident might involve. As public scrutiny of the sector rises, together with increased recognition of the scale of fraud and corruption risk facing such organisations, we need to move to a virtuous circle, fuelled by a desire to secure donor, public and staff trust by evidencing accountability and transparency. A virtuous circle might look like this:

As public scrutiny of the sector rises, together with increased recognition of the scale of fraud and corruption risk facing such organisations, we need to move to a virtuous circle, fuelled by a desire to secure donor, public and staff trust by evidencing accountability and transparency. A virtuous circle might look like this: